If one bank account receives your salary, pays your card bill, and holds your savings — can you say, right now, how much you can still spend this month? Most people can’t. When all your money sits in one place, budget lines become invisible. The simplest fix is a money system built on splitting your accounts: one account each for salary, spending, savings, and emergencies, with money moving to its place automatically the moment it arrives.

This guide walks through the four accounts in the money system, a 4-step setup that finishes the job on payday, a worked example on a KRW 3 million take-home salary, and the rules that keep the money system from collapsing after the first month.

Why you need a money system

With a single account, every won wears the same name tag. Rent money, next week’s groceries, and next year’s travel fund all blend into one balance — and when that balance looks even slightly comfortable, “I can afford this” comes far too easily. With a money system in place, the balance of your spending account simply is this month’s remaining budget. The limit is visible without any math.

Behavioral economics calls this mental accounting: people mentally sort the same money into different buckets, and those invisible buckets change how they spend. Richard Thaler, who won the 2017 Nobel Prize in economics, formalized the idea. A money system flips it to your advantage — it turns the buckets in your head into real accounts, attaching a physical label to every won.

The other half is automation. Once set up, a money system asks for no willpower. On the next business day after payday, automatic transfers carve out savings and the emergency fund first, and only the monthly budget lands in the spending account. The real shift is the order: not “save what’s left after spending,” but “spend what’s left after saving.”

Saving is not an act of willpower but of structure. A money system is the structure that sends every won to its place on payday — by itself.

The 4 accounts in your money system

Four accounts are enough to start. You can slice finer later, but every extra account adds management overhead, and overhead is what makes people quit. Here is what each account does.

① Salary account — the hub where income lands and bills leave

This is the account that receives your salary and pays the fixed costs — rent, building fees, telecom, insurance premiums, loan payments — that hit the same amount every month. Everything flows through here, so it acts as the hub of the money system. In Korea, salary-deposit history often unlocks preferential loan rates and fee waivers, so keeping this at your main bank usually pays off.

② Spending account — the boundary line of variable costs

This account holds only variable spending — food, transport, shopping, leisure. Link your debit card here and transfer in exactly one month’s budget. This is where the money system feels most powerful day to day: the balance equals what’s left of this month’s budget, so every glance at your banking app is a built-in spending check.

If you mainly use a credit card, add one more rule. Either move the same amount from the spending account to the card-payment account the moment you spend, or cap the card’s monthly limit in the card app at or below your spending budget. Set the card payment date after payday and your auto-transfer day, and check each month that the upcoming bill doesn’t exceed the spending budget.

③ Savings & investing account — the money you take out first

On payday, a fixed amount moves here before anything else. It collects installment-savings deposits and money headed to investment accounts. If you use products that auto-debit monthly, you can point this step straight at the savings product itself. For how to choose between a lump-sum deposit and installment savings in Korea, see our savings deposit vs installment savings guide.

One caution here. This account is only a transit hub — what your money actually becomes depends on the product it lands in. For deposits and installment savings, check whether they are covered by deposit protection; funds, ETFs, and stocks carry the possibility of principal loss, so it’s safest never to mix your emergency fund with investment money.

④ Emergency account — the safety valve of the system

Family events, hospital bills, sudden repairs — when an unexpected expense hits, this account absorbs it so you never raid your budget or break a savings product. A parking account (a free-withdrawal deposit you can tap anytime) fits best. Note that parking accounts differ by product: the balance cap that earns the headline rate, preferential conditions, the interest payout cycle, and deposit-protection status all vary, so read the product disclosure before signing up. You can compare rates and terms through the banking and savings-bank federations’ disclosures or each institution’s product documents. Also remember that brokerage CMAs, MMFs, and RPs — often used as parking-account substitutes — may be investment-type or performance-linked products rather than deposits, and may fall outside deposit protection. Before using one for your emergency fund, always check the deposit-protection status in the product disclosure. We covered how big your fund should be in how much emergency fund you really need.

| Account | Core role | What it holds | Recommended form |

|---|---|---|---|

| Salary (hub) | Receives income, pays fixed bills | Rent, fees, telecom, insurance | Main-bank checking account |

| Spending | Caps variable spending | Food, transport, shopping, leisure | Checking account + debit card |

| Savings & investing | Pay-yourself-first money | Savings and investment deposits | Savings products, brokerage |

| Emergency | Buffer for surprises | Target: 3–6 months of expenses | Deposit-protected parking account |

Once the money system has settled in for two or three months, you can add a fifth account: a purpose account for expenses that hit once or twice a year in lump sums — travel funds, holiday and family-event money, car insurance premiums. Divide the expected annual amount by 12 and set it aside monthly, and those lump sums will never touch your emergency fund or monthly budget. Just don’t rush it — expand only after the basic four accounts feel routine.

Set up your money system in 4 steps

Step 1 — Split 2–3 months of spending into fixed and variable

Every money system starts with knowing your real numbers. Pull the last two or three months from your card statements and bank history, then sort everything into fixed costs (rent, telecom, insurance) and variable costs (food, shopping, leisure). If this is your first time, the sorting method in our 3-step budgeting system works as-is. The fixed total is what stays in the salary account; the variable average becomes the spending account’s budget.

Step 2 — Assign roles to four accounts

You don’t need four new accounts. Reassigning roles to accounts you already own starts the money system today — keep the salary account as is, repurpose an idle account for spending, designate one parking account for emergencies. If you do open new ones, the process can be delayed by Korea’s restrictions on opening multiple accounts within a short period or by the financial-transaction-purpose verification step, and how these rules apply varies by institution and sector. Assign roles to existing accounts first, then open only what you need, one at a time.

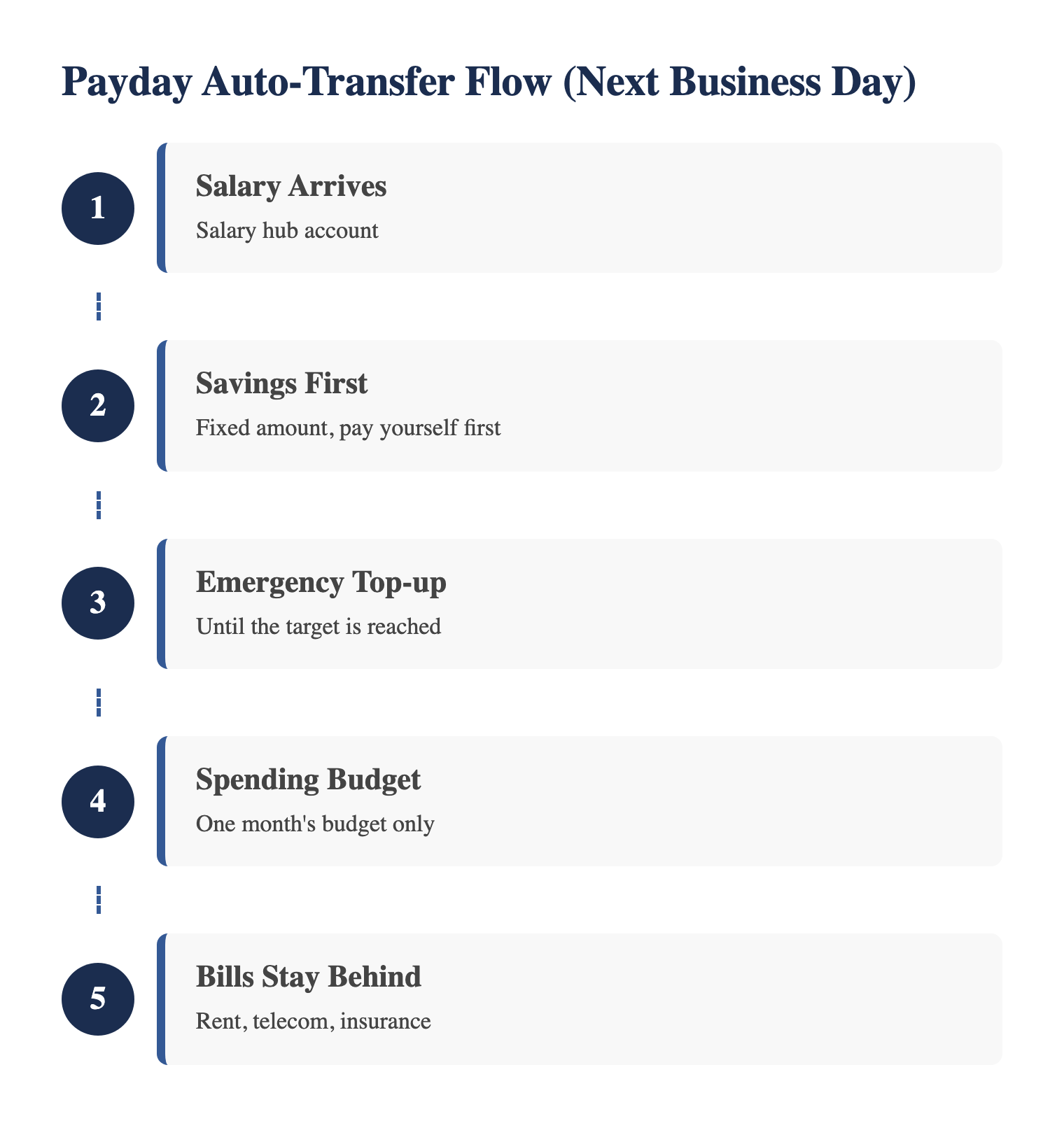

Step 3 — Chain your auto-transfers to the next business day after payday

Automatic transfers are the engine of the money system, and the order matters: savings & investing → emergency → spending, all scheduled for the next business day after payday. Salary deposits can land late in the day, and if the following day is a weekend or holiday the transfer schedule can slip — so set your auto-transfer date around your actual salary-deposit pattern. Within a day or two of getting paid, every won has found its place, and only fixed bills remain in the hub.

Step 4 — A 10-minute month-end check and a leftover rule

At month-end, spend ten minutes on the spending account balance. If money is left, sweep it to the emergency account; if you ran short, adjust next month’s budget. “Leftovers go to the emergency fund” keeps the money system alive far longer than “leftovers are my reward.” Once the emergency fund reaches its target, decide in advance where leftovers go next — a purpose account or the savings & investing account. After two or three months you’ll see your household’s true variable average — reset the budget to that number and the system is complete.

A money system example on KRW 3M take-home pay

If you don’t know where to set the ratios, start from the 50-30-20 budget rule: on KRW 3,000,000 take-home, that’s 50% needs (1.5M), 30% wants (0.9M), and 20% saving and investing (0.6M).

One caveat before the table: the two classifications are not identical. 50-30-20 sorts spending into needs / wants / saving, while the money system manages money by fixed / variable / saving / emergency. Groceries and commuting costs are variable but can be needs; an OTT subscription is a fixed cost but clearly a want. On KRW 3M take-home, the 50% (1.5M) covers fixed needs and variable needs combined, and the 30% (0.9M) is discretionary spending. In practice, you can adjust by keeping fixed needs in the salary account and putting variable needs plus the discretionary budget together in the spending account.

The table below takes the 50-30-20 numbers as a starting point and rearranges them into fixed costs, spending, savings, and emergency for actual account management. The spending account’s KRW 0.9M can hold variable needs (food, commuting) and discretionary spending (leisure, shopping) together — so in practice, adjust the amounts to match your own card statements.

| Account | Monthly allocation | Detail |

|---|---|---|

| Salary (hub) | KRW 1.5M stays | Pays rent, fees, telecom, insurance |

| Spending | KRW 0.9M transferred | Food, transport, leisure (debit card) |

| Savings & investing | KRW 0.4M transferred | Savings products and investments |

| Emergency | KRW 0.2M transferred | Until the target is reached, then redirected to savings |

Set the emergency target from monthly expenses: here, fixed 1.5M + variable 0.9M = KRW 2.4M a month, so three months of cover is KRW 7.2M. At 200,000 won a month that takes a while — so when irregular income arrives (a bonus, a year-end tax refund), send it to the emergency account first to reach the target faster. Once it’s full, redirect that 200,000 won to savings and investing and let your saving rate climb.

These ratios are a starting point, not a verdict. A single-person household with heavy housing costs may run needs above 50%; a family’s saving capacity differs again. What matters in a money system is not the textbook ratio but fixing your numbers per account and letting auto-transfers enforce them.

3 reasons a money system breaks — and the fixes

Starting a money system is easy; keeping it is the hard part. Collapses almost always follow one of three patterns.

- Covering overspending with the emergency fund: the moment the emergency account becomes “spending account #2,” the system is gone. Keep a hard rule — emergencies only — and handle overspending by deducting it from next month’s budget instead.

- Scattered transfer dates: when transfers fire on different days, one insufficient balance breaks the chain, and a broken chain rarely gets rebuilt. Unify everything on the next business day after payday, and move card payment and utility dates after it where possible.

- Ignoring fee waivers and rate changes: transfer fees between accounts are a recurring tax on your money system. Confirm fee-waiver conditions first. For time deposits and installment savings, compare current rates on the FSS Finlife deposit rate comparison; parking-account (free-withdrawal deposit) rates have limited consolidated disclosure, so check the banking and savings-bank federations’ disclosures or each institution’s product documents before choosing.

On deposit protection: spreading money across institutions can help compared with concentrating a large sum in one place. Since September 1, 2025, Korea’s deposit protection limit is KRW 100 million per person per financial institution, principal and interest combined (Financial Services Commission announcement). Keep in mind that protection covers eligible deposits only — funds, MMFs, brokerage CMAs, RPs, and other investment-type or performance-linked products may not be protected, so check the deposit-protection status in each product’s disclosure.

Closing — structure beats willpower

The essence of the money system is not the number of accounts but the reversal of order: from “save what survives the month” to “spend what’s left after saving” — enforced by automatic transfers, not resolve. Setup takes an hour or two once; after that, a ten-minute month-end check is all the maintenance the money system needs.

Your task today is a single one: before your next payday, schedule one automatic transfer into the savings account. The amount can be small. A money system doesn’t begin with a perfect plan — it begins with the first transfer.

Disclaimer: This article is for informational purposes only and does not recommend any specific financial product or institution. Interest rates, preferential conditions, fees, deposit-protection status, and account-opening policies vary by institution and change over time — before signing up, verify the latest terms on the FSS Finlife comparison site, in the banking and savings-bank federations’ disclosures, or in each institution’s app or product documents.