On the same KRW 300 million borrowed over 30 years, a 1 percentage-point change in your loan rate can shift total interest by tens of millions of won. So should you lock in a fixed rate or ride a variable one? Bank officers often default to “fixed is safer,” but the right answer depends on your loan duration, the rate outlook, and whether you expect to repay early.

This guide breaks down how Korean loan rates are built, the real differences between fixed and variable rates, a concrete simulation on a KRW 300M 30-year mortgage, and five practical decision factors. Thirty minutes of homework before you visit the bank can change the amount of interest you pay over a lifetime.

How a Korean Loan Rate Is Built

The headline “4.2% APR” you see in a Korean bank ad is actually the sum of three moving parts. The formula: loan rate = base rate + spread − preferential discount. Once you understand each part, the differences between competing bank quotes stop looking random.

The base rate represents the bank’s funding cost. Variable-rate mortgages and jeonse loans are usually tied to COFIX (Cost of Funds Index), while variable credit loans track 6-month or 1-year financial bond yields. Both follow the Bank of Korea base rate with a short lag (BoK base rate history).

The spread is the margin the bank adds for your individual credit risk plus its operating costs. Lower credit score, weaker collateral, or higher loan-to-value ratio push the spread up. The preferential discount is a rebate you earn by meeting behavioral conditions — salary deposit, card usage, auto-pay registrations — each worth 0.1 to 0.3 percentage points, typically stacking up to 0.5–1.0%p off the final loan rate.

Because the spread keys off your credit score, spending a few months on habits that raise your credit score before applying usually beats chasing preferential-rate conditions after the fact.

Fixed vs Variable: Head-to-Head Comparison

A fixed-rate loan locks in the rate at origination for the entire term. A variable-rate loan resets at every interval (typically 3, 6, or 12 months) based on the current base rate. In practice, most Korean mortgages today are mixed-type products — fixed for the first five years, then variable — tied to a 5-year financial bond yield.

| Factor | Fixed Rate | Variable Rate |

|---|---|---|

| Initial rate | 0.3–0.7%p higher than variable | Lower at start |

| Rate-hike risk | None (locked in) | Reprices each interval |

| Early-repayment fee | Typically higher | Relatively lower |

| Payment predictability | Very high | Lower (monthly amount varies) |

| Best for | Long-term, rising-rate period | Short-term, falling rates, early payoff |

The initial spread between fixed and variable is usually 0.3–0.7 percentage points. Fixed looks more expensive at signing, but once you ride through a 1–2%p rate-hike cycle over 10+ years, fixed often wins on cumulative interest. Conversely, in a falling-rate period — or if you plan to repay within five years — variable is almost always cheaper.

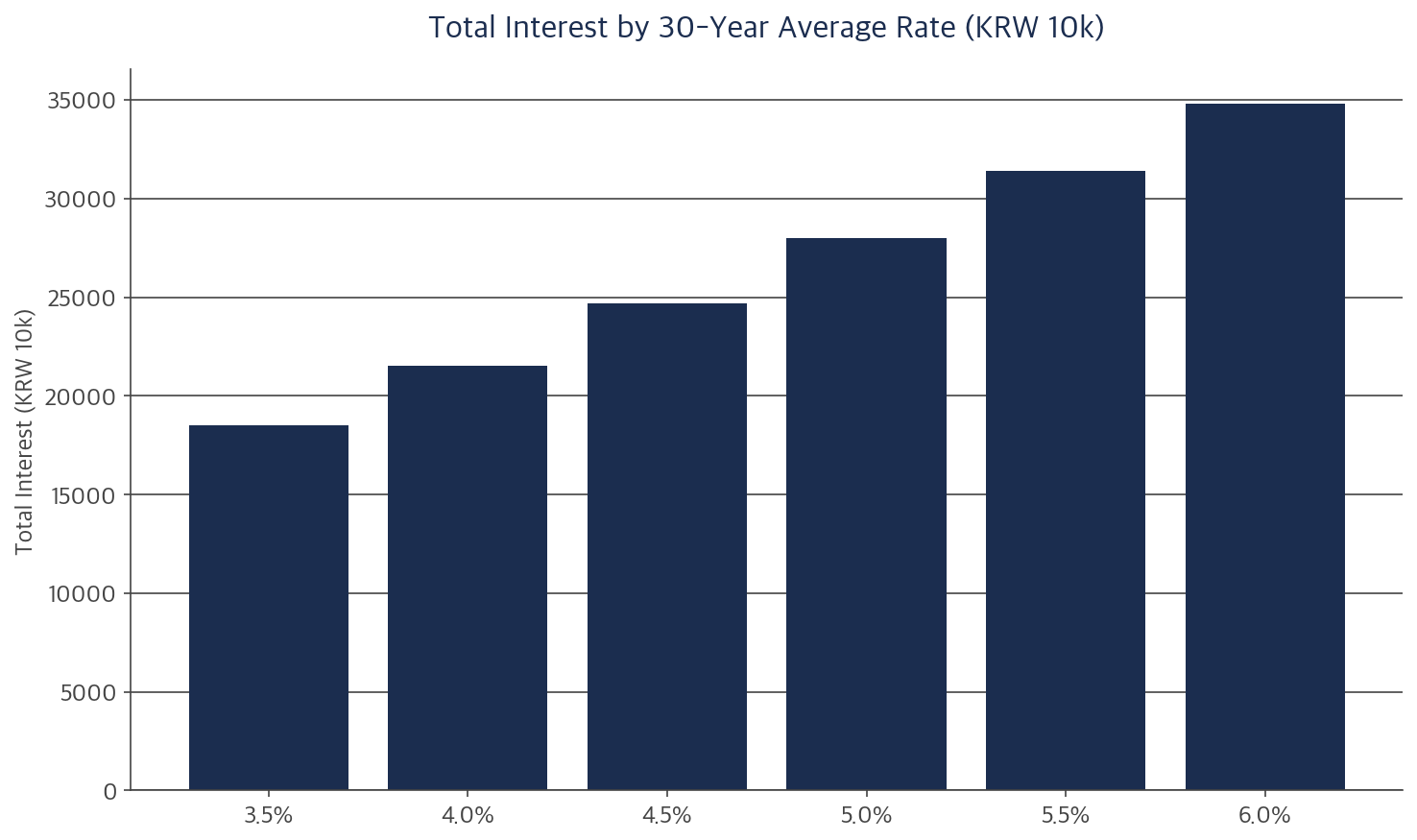

KRW 300M over 30 Years: What the Loan Rate Really Costs

Percentages feel abstract until you see won. Here is a concrete simulation: KRW 300 million borrowed for 30 years on an equal-installment (principal+interest) schedule, showing how total interest moves with the average loan rate over the life of the mortgage.

At an average 4.0%, total interest lands around KRW 215 million. Shift that average up to 5.0% and total interest jumps to roughly KRW 280 million — a single percentage point equals about KRW 65 million over 30 years. This is why paying 0.3%p more up front for a fixed loan rate can still be a net win if it shaves the long-run average.

The flip side matters too. If your loan term is only 5–7 years or you plan to repay early, you never experience the long-run average, so the initial rate differential dominates. That normally favors variable. The first question to answer isn’t “fixed or variable?” — it’s “how long will I actually carry this debt?”

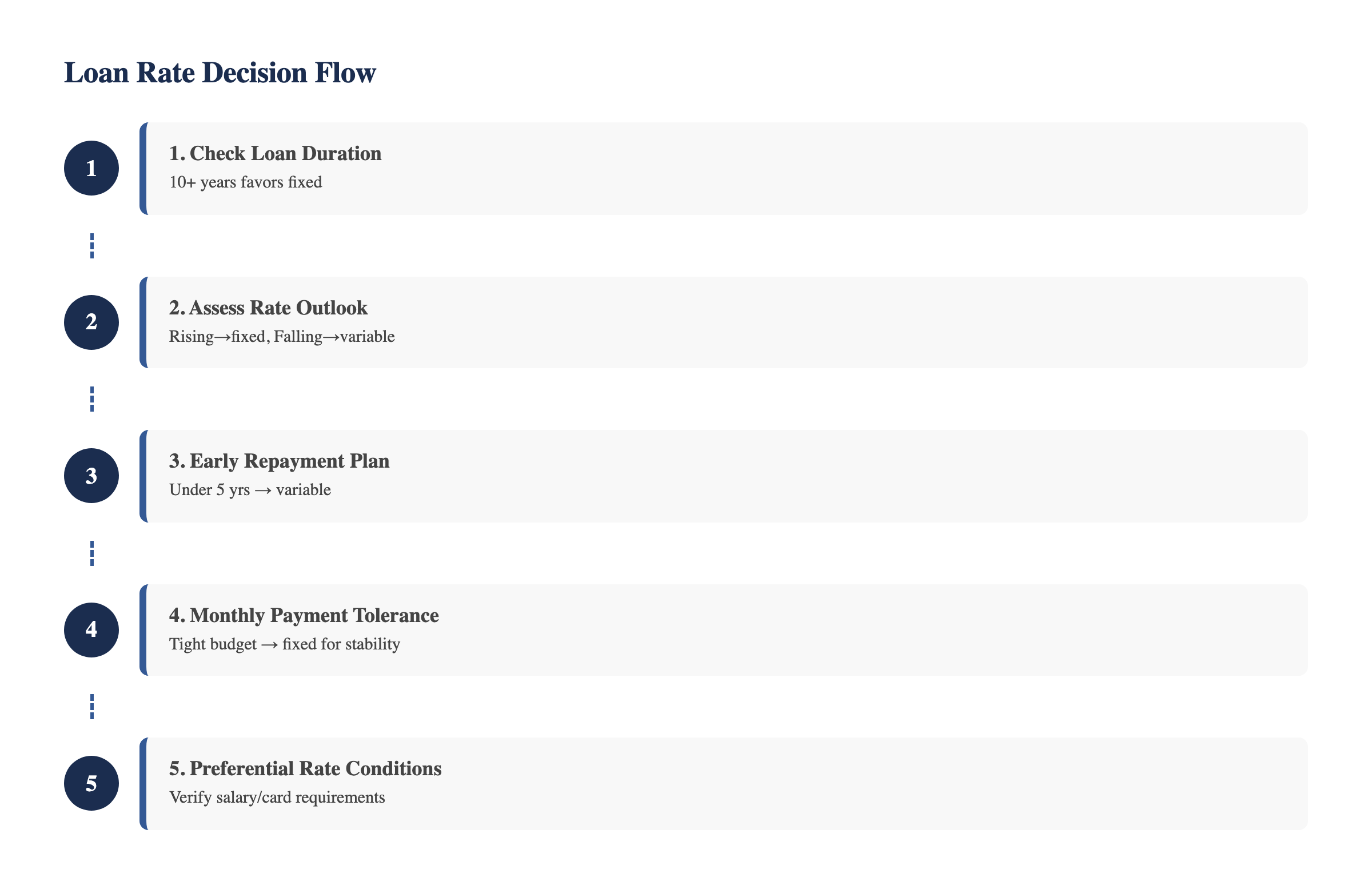

Five Factors for Choosing Your Loan Rate

Walk through these five questions in order. They will tell you whether fixed, variable, or mixed fits your specific situation.

1. Duration: tilt to fixed if the loan runs 10+ years

On a 30-year mortgage, you will almost certainly ride through at least one rate-hike cycle. Paying 0.5%p more for fixed (or a 5+ year mixed product) to neutralize that risk usually pays off. For a 3–5 year credit loan, variable is fine — the worst-case upward drift is modest, and you can refinance quickly.

2. Rate outlook: fixed when rising, variable when falling

Read the Bank of Korea’s monetary policy statement and the Monetary Policy Board minutes for directional signals. If market consensus leans toward hikes, locking in with fixed is the safer bet. If cuts look imminent, a variable loan rate captures the decline. Rate forecasts miss often, though, so anchor decisions on your own tolerance, not on expert predictions.

3. Early repayment: go variable if you’ll pay off within 5 years

Fixed-rate loans usually charge 1.2–1.4% early-repayment fees versus 0.7–1.0% on variable, with Korean banks typically waiving both after three years. If you might sell the property or make a large prepayment within 2–3 years, variable’s lower fee structure is a clear win.

4. Monthly budget: fixed when cash flow is tight

If your debt-service ratio (DSR) exceeds 35%, a variable loan rate that resets higher can destabilize your household budget. In that situation, paying slightly more up front for fixed buys you predictability — which is often worth the premium. When cash flow is roomy, variable saves on the front end and you can handle any rate increases with partial prepayments or refinancing.

5. Preferential rate conditions you can actually maintain

Whether you pick fixed or variable, meeting all preferential-rate conditions can trim another 0.5–1.0%p off your loan rate. Common conditions — salary deposit, monthly credit card spend of KRW 300,000+, three or more auto-pay setups — need to be sustainable year after year. If you drop a condition a year in, your rate spikes back up at the next review.

Practical Loan Rate Comparison Tips

A single bank quote tells you nothing about what a reasonable loan rate looks like. You need at least three to spot the spread differences. The most efficient shortcut is the Financial Supervisory Service’s unified comparison portal.

- FSS Financial Product Lookup: finlife.fss.or.kr mortgage comparison shows each bank’s average and lowest loan rate, split by fixed vs variable, on one screen.

- In-app rate inquiry: Korean bank apps let you request a rate quote without a hard credit pull, so you can compare without damaging your score.

- Know “mixed” vs “pure fixed”: A “5-year fixed, then variable” product switches to variable in year six. If you want fixed for the full 30 years, confirm the product is labeled pure fixed, not mixed.

- Document preferential conditions: After a bank consultation, ask for the preferential-rate conditions in writing. This protects you if the bank changes the terms a year later.

- Review refinancing options annually: If your current loan rate is 1%p or more above the market, refinancing may cut interest significantly. Korea’s online refinancing infrastructure often allows switching without large transfer fees.

Frequently Asked Questions

How do COFIX and financial bond rates differ?

COFIX is a weighted average of funding costs at eight major Korean banks (deposits, savings products, financial bonds), published on the 15th of each month. It comes in two flavors — “new-business basis” (more volatile) and “balance basis” (smoother). Financial bond yields trade in the market in real time, so they react faster to Bank of Korea moves. Variable mortgages usually track COFIX; variable credit loans track 6-month or 1-year financial bond yields.

What are the tradeoffs of a mixed-type (5-year fixed then variable) loan?

You get five years of predictable payments, then shift to variable and benefit from any rate declines after year six. Mixed products typically carry a loan rate 0.1–0.2%p below pure fixed, which is why they dominate the Korean mortgage market. The downside: if rates are elevated when the switch kicks in, your payment can jump more than expected. Plan for the year-six transition as part of the decision, not after the fact.

When are early-repayment fees waived?

Most Korean banks waive the early-repayment fee once the loan has run for three years. Before that, the fee is prorated based on remaining term. Fixed loans carry higher fees because the bank already sold the expected interest stream to investors. If there’s any chance you’ll prepay, check the exact fee schedule and waiver date in the contract before signing.

How much does credit score change my loan rate?

At the same bank on the same product, the gap between a top-tier score (900+) and a mid-tier score (700s) can easily be 1.0–2.0 percentage points. On a KRW 300M 30-year mortgage, that translates to KRW 60 million or more in extra interest. Spending 3–6 months before applying on basics — paying the card bill on time, clearing delinquencies, paying down small loans — is the single highest-return tactic for cutting your loan rate.

Wrapping Up

The loan rate question doesn’t reduce to “fixed is safe, variable is cheap.” Run through the five factors — duration, rate outlook, repayment plans, budget tolerance, preferential conditions — with your actual numbers, then pick fixed, variable, or mixed accordingly. On a KRW 300M 30-year mortgage, a 1%p difference in your average loan rate means over KRW 60 million in interest, so a few hours of quote comparison can earn more than a year’s salary.

Always cross-check your bank quote against at least two competitors plus the FSS public comparison portal. For large, long-term loans, a second opinion from an independent financial advisor (on top of the bank officer) is one of the cheaper forms of insurance you can buy.

Disclaimer: This article is for informational purposes only and does not constitute a loan recommendation or investment advice. Loan rates, fees, and preferential conditions change frequently and vary by bank; always confirm current terms with the lending bank and the FSS comparison portal before signing any agreement.