In June 2026, investors everywhere are watching one company. The SpaceX IPO — the public listing of Elon Musk’s rocket company, Space Exploration Technologies Corp. — is scheduled for June 12 on the Nasdaq under the ticker SPCX. At roughly $75 billion raised, it would be the largest IPO in stock market history. Yet the moment you ask “Can I actually subscribe to it?” things get complicated, especially from Korea. This guide lays out the key facts of the SpaceX IPO and the realistic routes an investor in Korea can actually take. (As of June 2026 · last updated 2026-06-08 · pre-listing offering stage.)

Here’s the bottom line: a regular retail investor in Korea will struggle to get a SpaceX IPO allocation the way a domestic subscription works. Korean brokers did not open a subscription window, and the U.S. retail channels generally assume a U.S. residence and account. That said, you are not entirely shut out — the two realistic routes are buying SPCX after it lists on June 12, or taking indirect exposure through U.S. funds that already hold SpaceX. This article walks through those routes — their structure, cost, and risk — one by one.

SpaceX IPO: Where Things Stand

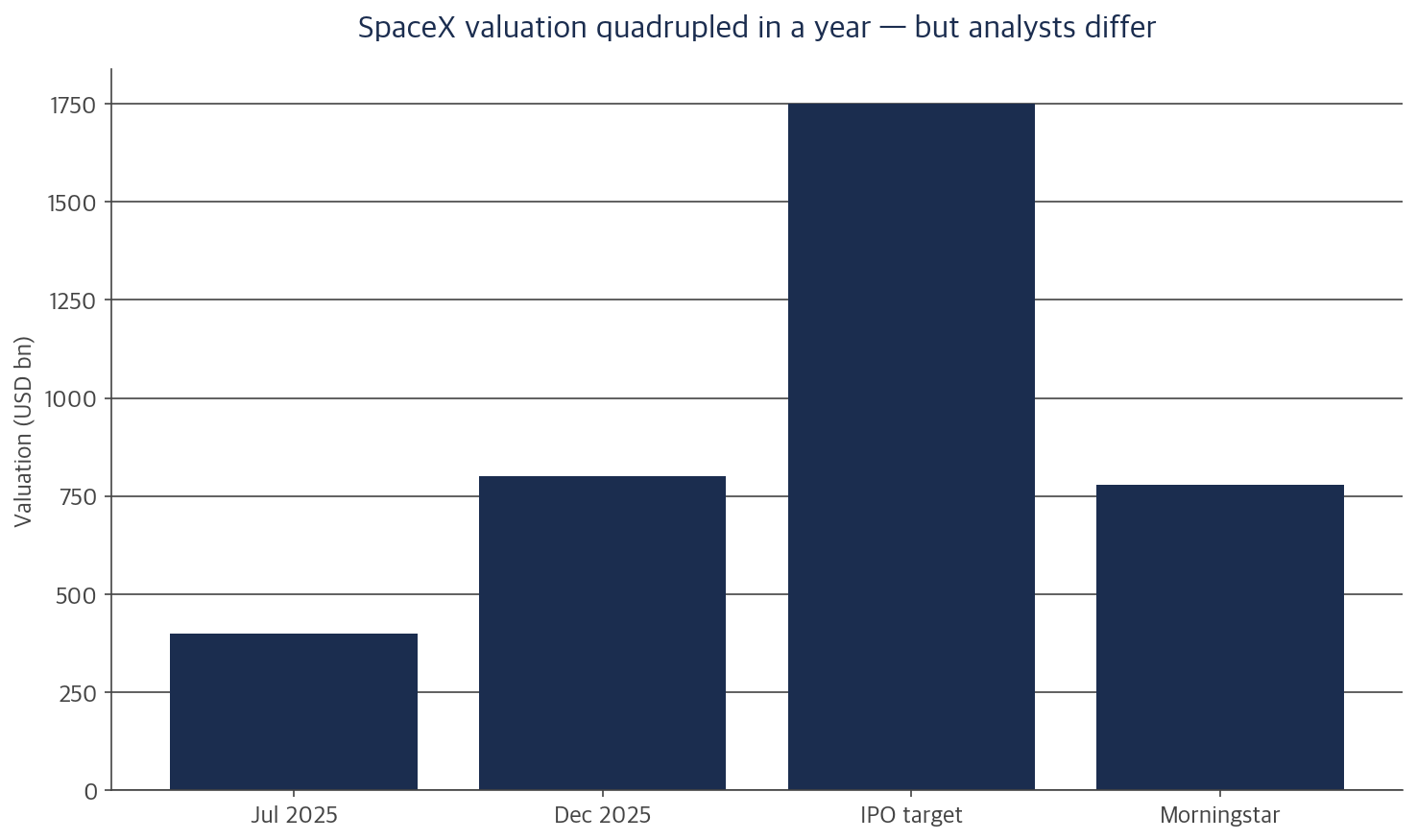

Start with the facts. SpaceX filed confidentially with the U.S. Securities and Exchange Commission (SEC) on April 1, 2026, then made its prospectus (Form S-1) public on May 20. The institutional roadshow began June 4, the price is fixed after the close on June 11, and the stock lists on the Nasdaq on June 12. The price marketed so far is $135 per share (about 210,000 won at roughly 1,550 won to the dollar, as of 2026-06-08).

On the base deal, the company plans to sell about 555.56 million shares to raise roughly $75 billion (about 116 trillion won); if the underwriters’ over-allotment option (up to 83.33 million shares) is exercised, the actual share count and proceeds could be larger. At that price the valuation reaches about $1.75 trillion (about 2,700 trillion won), and if it goes through it would be the largest IPO in U.S. market history. After the listing, Musk is reported to keep more than 80% of the voting control. Note, though, that the $135 is an indicative price, not the final one — the final offer price is set after the offering process and could be higher, lower, or the same. Confirm the actual terms in the SEC final prospectus and your broker’s notice.

| Item | Detail |

|---|---|

| Legal name | Space Exploration Technologies Corp. (SpaceX) |

| Exchange / Ticker | Nasdaq, SPCX (Class A common stock) |

| Pricing (expected) | June 11, 2026 (after close) |

| Listing date | June 12, 2026 |

| Marketed price | $135 per share (pre-final indicative) |

| Offering size | ~555.56M shares (+ over-allotment) · ~$75 billion |

| Target valuation | ~$1.75 trillion |

But look past the headline numbers. SpaceX revenue grew fast to about $18.7 billion in 2025, yet its accounting operating result was a loss of roughly $2.6 billion. By contrast, adjusted EBITDA was positive at about $6.6 billion — so the accounting result and the adjusted metric point in different directions. And some analysts disagree sharply on price: Morningstar pegs fair value at about $780 billion — less than half the IPO target. The same company is valued more than two-to-one apart depending on who you ask.

Why an Allocation Is Hard to Get in Korea

The biggest question about the SpaceX IPO in Korea is simple: “Can I subscribe to the offering?” The honest answer is that a general retail investor in Korea will find it hard to get an allocation the way a domestic subscription works — and the reason lies in both the U.S. and Korean systems.

Start with Korea. According to the prospectus and Korean media analysis of it, SpaceX designated some countries — Japan, the U.K., Switzerland, Canada, Australia — for a general “public offering,” but opened Korea only to a “private placement” aimed at professional and institutional investors. SpaceX stated that its Class A common stock is not registered as a public offering under Korea’s Capital Markets Act, and that it has no plan to register it.

Interestingly, this IPO is unusually generous to individuals. Reports say up to about 30% of the offering is earmarked for retail investors, and in the U.S., brokers such as Robinhood, Fidelity, and Charles Schwab let individuals request an allocation at the same price and the same time as institutions. Even so, an allocation is not guaranteed — the amount you actually receive depends on account requirements, country of residence, and demand.

The catch is that this retail channel generally assumes a U.S. residence and a U.S. brokerage account. Korean brokers did not open a subscription window for this deal, and Korea, as noted, is limited to private-placement access. So a general retail investor in Korea will struggle to get the marketed price the way a domestic subscription works. It is not that “every individual is absolutely barred,” but apart from exceptional, high-risk routes — a professional-investor private placement, some overseas brokers, or tokenized products — the realistic path for most individuals is to buy on the market after listing. (There is also a directed program of about 5% for employees and certain “friends and family,” but that is for insiders, not the general public.)

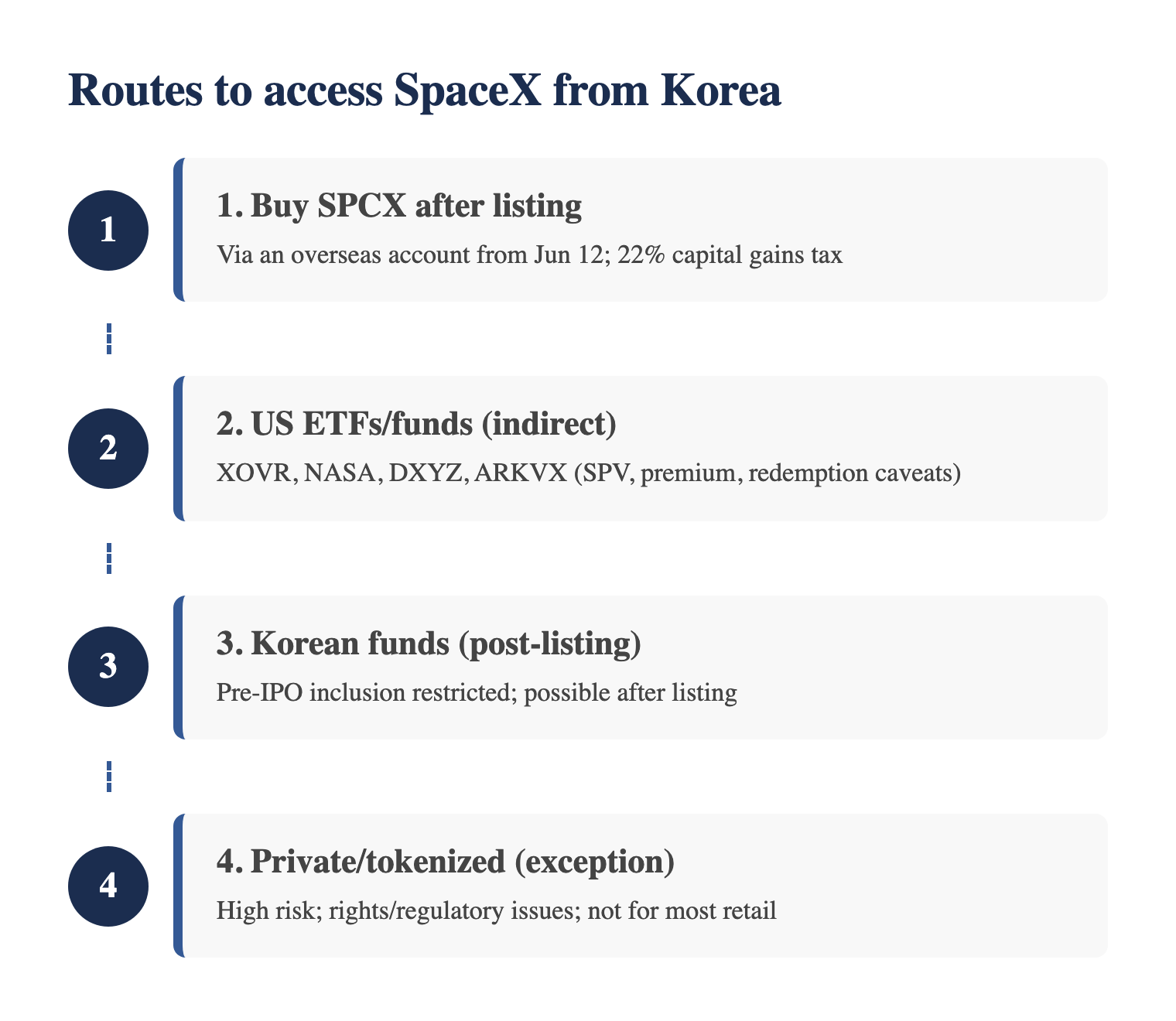

Routes to Access SpaceX from Korea

A hard SpaceX IPO allocation does not mean there is no road in. Access from Korea splits into four broad routes, in roughly descending order of suitability for an ordinary individual. Get the big picture from the flowchart first.

1. Buy SPCX Directly After Listing

This is the simplest route. Once the SpaceX IPO lists on June 12, you can buy SPCX through an overseas (U.S.) stock account. But “anyone with an account, instantly” is too simple. Korean brokers differ in when they register a newly listed ticker for trading, in whether you can order in the pre-market, regular, or after-hours session, in whether they support fractional shares, and in their currency-exchange hours and trading fees. It may not be tradable on day one at your broker, so check their guidance in advance.

Prepare for the price, too. On the first trading day, the market price can open above or below the $135 marketed price. The hotter the IPO, the bigger the day-one swings, so many advisers suggest scaling in rather than buying everything at once.

Plan for tax. Gains on U.S. stocks fall under Korea’s foreign stock capital gains tax: after an annual basic deduction of 2.5 million won, the remaining gain is taxed at 22% (20% capital gains plus 2% local income tax), and you file and pay it yourself during the capital-gains final-return period the following May. The full mechanics are covered separately in our foreign stock tax guide.

2. Indirect Exposure Through U.S. ETFs, Closed-End and Interval Funds

If you want exposure before the SpaceX IPO lists, you can buy U.S.-listed ETFs and funds that already hold SpaceX. The vehicles differ, though: XOVR and NASA (listed ETFs) and DXYZ (an NYSE-listed closed-end fund) may be tradable through a Korean overseas brokerage account — check with your broker — but ARKVX is an unlisted interval fund, so it may be hard or impossible to buy through an ordinary overseas account and needs separate checking. The names most often discussed are below.

| Fund (Ticker) | Type | SpaceX exposure (as of) | Key caveat |

|---|---|---|---|

| XOVR (ERShares) | Nasdaq ETF | Indirect via ‘SPV Exposure to SpaceX LLC’ (~22–23%) | Not direct ownership — exposure runs through an SPV |

| NASA (Tema) | NYSE-listed space-theme ETF | Indirect via a Forge SPV (e.g. ~6.49% as of Jun 5, 2026) | Spread across the space industry; SpaceX is a portion |

| DXYZ (Destiny Tech100) | Closed-end fund (NYSE) | ~14.5% (economic exposure as of Mar 31, 2026) | Can trade at a steep premium to net asset value |

| ARKVX (ARK Venture) | Interval fund (unlisted) | Holds SpaceX — weight: check latest holdings | Limited redemptions; high cost (Class D net 2.90% / gross 3.49%, varies by class and date) |

※ These weights and exposures can change quickly with new inflows around the IPO, revaluations, lockups, and rebalancing. Verify the latest figures, with their reference dates, in each manager’s official materials before investing. Note also that most of these vehicles hold exposure indirectly through an SPV rather than the shares themselves. A closed-end fund like DXYZ can trade far above its true asset value when demand surges, and that premium can evaporate fast on news such as a listing delay or a lower price. ARKVX carries redemption limits and a high cost ratio. None of them is “SpaceX stock itself.” You can review how the XOVR ETF is structured on the manager’s (ERShares) XOVR page.

3. Possible Post-Listing Inclusion in Korean Funds and ETFs

First, be clear that Korean space/aerospace theme stocks and domestic theme ETFs are not “SpaceX equity itself.” They are theme exposure to the space supply chain, or the possibility of holding SPCX after it lists — which is different from investing in SpaceX directly.

By their legal structure, Korean ETFs cannot easily hold private (unlisted) shares, so they could not directly add SpaceX before the listing. Some Korean managers were reported to be able to place privately-acquired holdings into mutual funds or active products, but the actual inclusion and weight must be checked in each fund’s reports and holdings disclosures after listing. If you prefer a domestic product, the practical move is to wait and verify the actual holdings after the listing.

4. Private Placement, Tokenized IPO and Other Exceptional, High-Risk Routes (Caution)

The last group is the one we do not recommend for ordinary individuals. First, a private placement for those who qualify as professional investors, or access through some overseas brokers, may be discussed — but eligibility rules, supply limits, and redemption constraints are significant. Second, there are “tokenized IPO (tokenized stock)” products offered by some overseas crypto exchanges.

A tokenized product is not direct ownership of SpaceX stock. It is a derivative token designed to track the price; you may have no shareholder rights, no voting rights, no dividend rights, and no direct claim against the issuer (SpaceX), plus added credit, bankruptcy, and regulatory risk from the token issuer. Redemptions or trading can be halted. Beginners should not treat such products as a substitute for a SpaceX IPO subscription.

Risks to Weigh Before You Invest

The SpaceX IPO is a compelling story, but several risks deserve a cold look before any decision.

- Valuation debate: the IPO target (~$1.75 trillion) and some analyst estimates (~$780 billion) differ by more than two-to-one. You may be paying up.

- Accounting loss: revenue grows fast, but the 2025 accounting operating result was a loss (adjusted EBITDA was positive), with heavy ongoing spending on Starship, satellite connectivity, and space infrastructure.

- Early volatility and lockups: newly listed stocks swing hard, and supply pressure can appear when insider lockups expire after a set period.

- The catch in indirect products: ETFs, closed-end and interval funds add their own premiums, cost ratios, and redemption limits.

- Rights and regulatory risk in exceptional routes: private-placement and tokenized products have opaque rights structures and heavy regulatory and redemption risk.

- Currency: as a U.S. stock, won-dollar moves flow straight into your return.

- Concentration: pouring money into one stock or theme raises risk. For diversification basics, see our ETF investing guide.

Nasdaq-100 Inclusion — and Why I’m Waiting

Finally, a different angle from the four routes above. Under the Nasdaq-100 “fast entry” rule effective May 2026, a newly listed company whose market cap ranks in the index’s top 40 (roughly $100 billion or more) is exempt from the usual three-month seasoning requirement and can be added about 15 trading days after listing. At a discussed valuation near $1.75 trillion, SpaceX clears the market-cap bar easily, so on schedule a Nasdaq-100 addition around early July 2026 looks likely (the official announcement comes around the 10th trading day, so it is not certain until then). For contrast, the S&P 500 remains out of reach for now because of its profitability rule.

The key point: once a stock joins the Nasdaq-100, index-tracking ETFs like QQQ must hold SPCX. So anyone who already owns the Nasdaq-100 gets automatic, proportional exposure without buying SPCX separately.

Personally, this is exactly why I’m sitting out the SpaceX IPO itself. I already hold the Nasdaq-100 at a meaningful weight, so if the fast-entry rule pulls SpaceX into the index, the index ETF I already own gives me some exposure automatically. Rather than piling on extra indirect exposure through another ETF or fund — and rather than forcing my way into the heavy early volatility — I’d rather wait and see whether and when it is added.

In short, I’d rather let the index do the work than bet on a single stock. That is just my call given my existing portfolio and risk tolerance, though, not the right answer for everyone. If you hold little or no Nasdaq-100, or you want to bet on SpaceX more directly, the direct-buy or ETF routes above may suit you better. Decide based on your own situation.

Read the Structure, Not the Hype

The SpaceX IPO is a genuine event of its era, but the “largest IPO in history” headline and the fear of being left out are two different things. The more a company’s valuation splits two-to-one — and with its offer price not even final — the more it pays to enter because you understand the structure and the risk, not because everyone else is buying.

- Korean retail can rarely get the offer price like a domestic subscription — the realistic path is to buy after listing (June 12).

- If you buy SPCX directly, pre-calculate Korea’s foreign-stock capital gains tax (22% after a 2.5M-won deduction).

- Pre-IPO exposure runs through U.S. funds (XOVR, NASA, DXYZ, ARKVX) — check the SPV, premium, redemption, and cost first.

- Private-placement and tokenized routes carry heavy rights and regulatory risk — not for ordinary individuals.

- The IPO target and analyst estimates differ two-to-one and the price is not final — enter only once you understand the structure and risk.

Frequently Asked Questions (FAQ)

Are SpaceX and Starlink listing separately?

This SpaceX IPO is not a separate listing of the Starlink satellite business; it is the listing of the whole parent — SpaceX, with Starlink inside it. There was once talk of spinning off Starlink, and a future separate listing is a different question, so this IPO alone does not mean Starlink will never be listed on its own. Starlink is a major revenue driver; its subscriber base was reported to top 10 million as of the first quarter of 2026.

Should I buy on the first trading day?

You can, but be careful. Hot deals like the SpaceX IPO often swing wildly on day one, and the market price can be above or below the marketed price. Rather than going all-in at once, scale in and commit only an amount you can afford to lose.

So can Korean individuals get an allocation at the offer price?

A general retail investor in Korea will find it hard to get the marketed price ($135) the way a domestic subscription works. The U.S. retail channels (Robinhood, Fidelity, and so on) generally require U.S. residence and a U.S. brokerage account, and Korea is limited to a professional-investor private placement. It is not that every individual is absolutely barred, but the realistic path for most individuals is to buy on the market after listing.

Next step — for the tax that follows buying SPCX, read our foreign stock tax guide; to value the stock yourself, see how to read PER, PBR and ROE.

Disclaimer: This article is for information and investment-education purposes only and is not a recommendation to buy or sell any specific stock, ETF, or fund. The dates, marketed price, valuation, and fund weightings here reflect the offering stage as of June 8, 2026; the final offer price, schedule, valuation, and fund weightings may change as the listing proceeds. Note also that closed-end funds, interval funds, and SPV-based products can differ from ordinary listed stocks in liquidity, cost, and rights structure. Before investing, review primary sources directly, such as the SpaceX prospectus (Form S-1) filed with the SEC, each manager’s official materials, and your own broker’s guidance. All investment decisions are your own responsibility.